AZ Debt Settlement Solutions, debt elimination program, debt advice help, debt free

solutions, consolidating credit and debt, credit card debts, consumer debt reductions

for Phoenix, Tucson, Mesa, Glendale, Scottsdale, Gilbert, Tempe, Peoria, Surprise, Yuma, Avondale, Casas Adobes, Catalina Foothills, Flagstaff, Goodyear, Lake Havasu City, Buckeye, Maricopa, Oro Valley, Sierra Vista, Prescott, Casa Grande, Bullhead City, Sun City, Prescott Valley, Marana, Sun City West, Apache Junction, Drexel Heights, Kingman, Fountain Hills, San Luis, El Mirage, Queen Creek, Fortuna Foothills, Sahuarita, Florence, Green Valley, Nogales, Tanque Verde, Douglas, Flowing Wells, Payson, Arizona.

Debt Settlement

If you are engulfed in massive debt, paying your bills is

becoming more difficult and you want to stop annoying and intruding collection calls, debt

settlement may be a viable options for you. Also know as debt negotiation, debt

settlement is a process by which your outstanding debt is settled for 40%-60% of

the amount owed. By agreeing to this settled amount, the creditor is forgiving the

remaining debt, thereby helping the client get out of debt faster.

If you are engulfed in massive debt, paying your bills is

becoming more difficult and you want to stop annoying and intruding collection calls, debt

settlement may be a viable options for you. Also know as debt negotiation, debt

settlement is a process by which your outstanding debt is settled for 40%-60% of

the amount owed. By agreeing to this settled amount, the creditor is forgiving the

remaining debt, thereby helping the client get out of debt faster.

- The 4 Basic Steps in Debt Settlement...

- Client stops payment to creditors, and starts contributing to trust account.

- Collection calls are handled by the debt settlement representatives.

- Negotiation of debt happens a few months after program begins.

- Debt is lowered by 40%-60% in a overall shorter time period.

Brief History on Debt Settlement:

Lenders have been practicing debt settlement

concepts for hundreds of years. Creditors are usually willing to settle because it means

that they will receive some amount of money owed as opposed to nothing or very little if the

client files for bankruptcy. Debt settlement became prominent in America when bank

deregulation during the late 80s made lending to consumers easier. This deregulation

was followed by a recession which created financial hardships for consumers.

As individual consumer debts increased, banks established debt

settlement departments to negotiate with defaulted cardholders.

Changes to Bankruptcy Laws:

Not only have personal debt loads risen but another under reported change in 2005

has driven the demand for debt settlement. Legislation now has made it more difficult

for Americans to claim Chapter 7 bankruptcy. Currently anyone filing for bankruptcy

will be required to meet IRS regulations or will be forced into Chapter 13 which is

a debt restructuring plan.

Posted By: AZDebtSettlement.com |

Category: Debt Settlement | Topic: Debt Settlement

Bankruptcy

Many consumers that have considered bankruptcy have chosen

to utilize debt settlement once they learned what a tremendous

tool it can be for debt relief. Bankruptcy is never the only option. We consider not only the

qualifications of the client, but also the client objectives when determining which debt

relief strategy is the most appropriate. If the client does not qualify for debt settlement as

determined by our attorneys, one of our highly qualified bankruptcy lawyers will be

able to assist the client.

Many consumers that have considered bankruptcy have chosen

to utilize debt settlement once they learned what a tremendous

tool it can be for debt relief. Bankruptcy is never the only option. We consider not only the

qualifications of the client, but also the client objectives when determining which debt

relief strategy is the most appropriate. If the client does not qualify for debt settlement as

determined by our attorneys, one of our highly qualified bankruptcy lawyers will be

able to assist the client.

- Filing for bankruptcy usually requires the following...

- Undergoing a "means" test.

- Receiving debt counseling from an approved organization.

- Submitting a repayment plan.

- Attending a meeting with creditors.

There are two different types of bankruptcy. Chapter 7 allows a consumer to discharge

most debts without having to repay them. In order to qualify for Chapter 7 bankruptcy

a client cannot earn more than the average income for their state of residence.

Additionally, in order to qualify a client must be unable to pay more than $100 per

month to creditors after all reasonable expenses are accounted for. If a client does

not meet these and other requirements they will be forced to file Chapter 13 bankruptcy

which takes longer and requires the debtor to pay back a portion of debts owed. Filing for

bankruptcy will stop all collection activity but there are important

consequences to remember with either form of bankruptcy.

- Debtors can leave bankruptcy with heavy court and attorney fees.

- Assets including homes, businesses, autos, etc. may be taken as payment.

- Exploitation is required in front of a judge and creditors.

- Bankruptcy remains on the consumers credit report for up to 10 years.

Whether your situation dictates debt settlement or bankruptcy

we can help along the way. Complete our debt analysis form and we will help advise which path is best suited for you.

Posted By: AZDebtSettlement.com |

Category: Debt Settlement | Topic: Bankruptcy

Continue to pay the minimum

If minimum payments are made on credit cards with ridiculous interest rates

it may take 30+ years to get out of debt. In some cases it would take an average

of 6 years for every $3,000 of debt. This is definitely the method that credit card

companies prefer you choose. Unless you plan on making larger payments on your

debt or you plan on coming upon a large sum of money, the lack of debt relief strategy

will not only take a toll on you financially but emotionally and physically as well.

If minimum payments are made on credit cards with ridiculous interest rates

it may take 30+ years to get out of debt. In some cases it would take an average

of 6 years for every $3,000 of debt. This is definitely the method that credit card

companies prefer you choose. Unless you plan on making larger payments on your

debt or you plan on coming upon a large sum of money, the lack of debt relief strategy

will not only take a toll on you financially but emotionally and physically as well.

Even if you choose to do nothing the creditors will not take the same approach,

the harassing phone calls and repossessions will continue, along with other headaches.

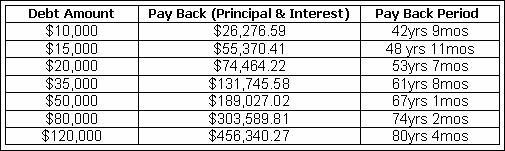

The chart below shows the length of time as well as the total amount paid if the

consumer continues to pay the monthly minimum. These assumptions are based

on a 19% interest rate and a monthly minimum of 2.1%.

(Most credit card minimums are between 2.0% and 2.5%)

Posted By: AZDebtSettlement.com |

Category: Debt Settlement | Topic: Continue to pay the minimum

Get A Free Debt Analysis

Click on the image below and fill out the form to have a debt specialist contact you for a free debt analysis and confidential consultation.

Debt Management

When a consumer becomes inundated with several credit cards and needs to

consolidate or needs help with high interest rates, debt management may be a

possible solution for the client. The typical debt management organization will

advise their clients to close their credit card accounts and instead pay a single

payment directly to the debt management program. The advantages are

that the debt management company takes care of paying each credit card and

negotiates the interest rate to shorten the length of time the client is in debt.

This type of program will typically take longer than a debt settlement program

because it still requires paying debts in full with interest.

Most of these companies are established and funded by lenders in order to

help collect as much debt from a client as possible. Non-profit organizations

have been scrutinized for funneling operating expenses back to the original creditor.

Also, these companies will report third party assistance (TPA)

on your credit report which can be as damaging as bankruptcy.

Be aware of companies that...

• Charge high up-front or monthly fees.

• Pressure for "voluntary contributions".

• Refuse program info without personal info.

• Try to enroll a client without qualifying them.

• Enroll a client without teaching budgeting.

• Enroll before creditors have accepted terms.

Consolidation Loans

Like many debt management programs, consolidation loans convert many different

payments into one payment every month by obtaining a single loan to pay

off all of the others. The idea is to help consumers keep track of their

finances and reduce the chance of late or missed payments.

Debt consolidation loans are classified as either secured or unsecured.

A secured loan required collateral such as a home. If the debtor cannot

make payments on a debt consolidation loan they run the risk of losing their

home. In converse an unsecured loan does not require collateral but usually

carries a much higher interest rate.

Debt consolidation loans are usually only possible when the consumer has a

low debt-to-income ratio and/or has a home to put up as collateral. It would

make sense for the consumer if they have multiple high interest rates on varying

cards and wanted to consolidate them into one lower monthly payment.

Some of the obvious issues with debt consolidation loans are a larger payback

sum and a much longer term, sometimes 10-20 years longer. Another effect is a lower

credit score due to the additional loan. A transaction fee paid upon closing or

built into the interest rate is another drawback. The other major issue is it does

not help the consumer who may still be struggling through a hardship. If the debtor

falls back on hard times they run the risk of defaulting on the consolidation loan

and losing hard earned assets put up for collateral. This means the costs of

missing a payment could be the debtor's home!